Download this Commentary (PDF)

View additional content on the Congressional Review Act.

In brief...

A new project at the Administrative Conference of the United States will consider technical reforms to the Congressional Review Act. The recently-issued draft report is an excellent primer on the details of regulatory agency and congressional staff implementation of the CRA. It provides a deep dive analysis of several policy options available to Congress to improve the CRA. ACUS is going through its process to develop draft recommendations now.

Introduction

A new project at the Administrative Conference of the United States (ACUS) will consider technical reforms to improve the implementation of the Congressional Review Act ( CRA). The agency put out a request for proposal earlier this year for a consultant to produce a report that would inform its recommendations. Outside of the detailed reports produced by the Congressional Research Service on this topic, the draft report for ACUS by Professor Jesse M. Cross is one of the most in-depth treatments of the procedural issues related to federal agency and congressional staff implementation of the CRA’s requirements. The report identifies three reforms as “potential good governance solutions” and discusses the tradeoffs among the policy options available to Congress to enact them. The areas under review include 1) the current practice of regulatory agencies hand-delivering reports to Congress, 2) the uncertainties related to timeframes for congressional action under the CRA, and 3) the procedure used by members of Congress for regulatory actions that were never submitted to Congress.

The draft report is well researched—drawing from academic work, written testimonies to Congress, and interviews with congressional staff. The report informs the November 4th draft recommendations (which are being deliberated in committee and will not be final until a full vote of the Conference). The November 4th draft recommendations by ACUS would propose:

- Streamlined reporting by regulatory agencies via electronic submission to Congress;

- A simplified process for determining relevant dates for congressional action;

- The codification of review by the Government Accountability Agency (GAO) in cases where agencies did not submit regulatory actions to Congress.

If finalized by ACUS, and then enacted by Congress, the proposed reforms could substantively improve the implementation of the CRA.

The Congressional Review Act in Brief

Congress enacted the CRA in 1996 to enhance congressional oversight of federal agency rulemaking. As I have elaborated elsewhere, the CRA provides Congress with a mechanism to eliminate final rules issued by federal agencies with a simple majority vote in both houses and “fast track” procedures for the Senate—which includes the ability for 30 senators to make a non-debatable motion to move resolutions to the floor while preventing any dilatory actions (i.e., the filibuster). Once a resolution of disapproval under the CRA becomes law the agency rule in question is nullified and the agency is prevented from reissuing any rule “in substantially the same form.”

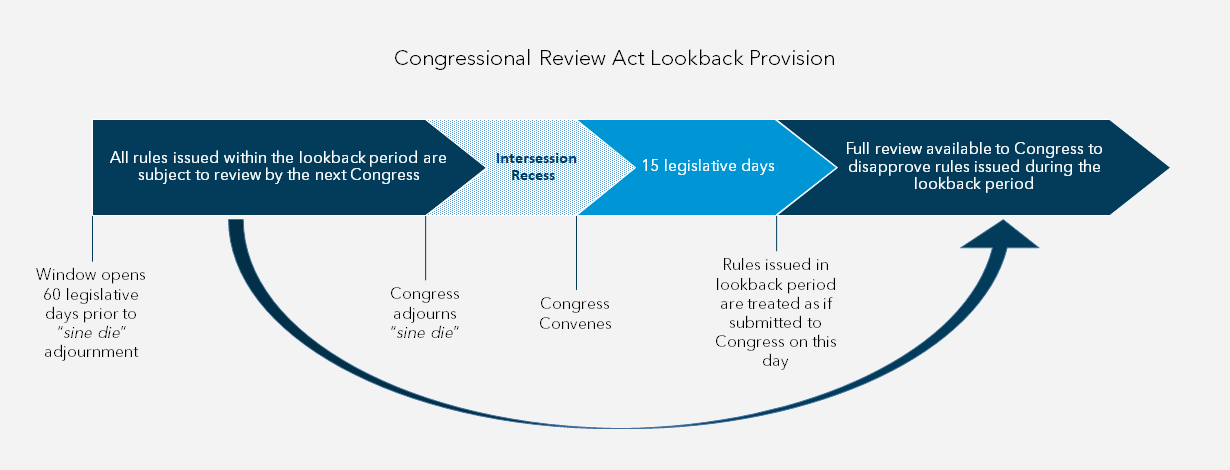

Although this oversight function is relatively straightforward, understanding and implementing congressional review under the CRA is fairly complex due to the Act’s use of various overlapping timeframes for introducing and acting on resolutions (often different for each chamber). The CRA also contains a lookback provision allowing a subsequent session of Congress to disapprove any rules agencies issued during the final 60 working days of a previous Congress. The review window associated with the lookback provision cannot be precisely calculated until the end of a Congressional session, which adds substantial uncertainty surrounding the number of agency actions that will be eligible for expedited oversight in a subsequent Congress. Additionally, the CRA states that before a rule can take effect, federal agencies must submit a report to each house of Congress and the Comptroller General (the head of the GAO). Submission to Congress is important because it affects the timeframe for expedited congressional review under the CRA.

{kind=link}

Streamlining Submissions of Agency Reports to Congress

The CRA does not specify how agencies should submit reports to Congress, but existing congressional rules necessitate that they hand-deliver these reports to Congress. Hand delivery intuitively seems like it would be more burdensome than electronic submission, but recent events have illustrated concerns about the reliability of this method of submission. For example, the COVID-19 pandemic has made it such that more employees have flexible work arrangements (i.e., staff may not be present to send or receive hand-delivered reports). Additionally, the events of January 6 led to the office of the Senate parliamentarian being ransacked by rioters which caused delays in processing reports submitted by agencies. All of this suggests that an ACUS recommendation to switch to electronic submission would be an improvement over the status quo.

Simplifying Time Periods for Congressional Oversight

My own experience writing about the CRA has taught me that identifying review periods and deadlines requires a nontrivial amount of subject matter expertise. This is perhaps the most difficult issue the report grapples with—the complexity inherent in calculating the review periods available to Congress. Notably, any change regarding how dates are calculated would affect the number of rules subject to CRA oversight—particularly when it comes to the Act’s lookback provision. That is, changes that effectively shorten or lengthen review periods are as much a political question as a policy one. Nonetheless, the report relies on historical data to provide a sober assessment of various actions Congress could take to reduce the uncertainty of timeframes related to review periods. As far as the lookback provision, the November 4th ACUS draft recommendations encourage Congress adopt a fixed date for the start of the lookback period such that any rules submitted to Congress after this date would be subject to expedited review under the CRA during the next session of Congress.

Formalizing GAO’s Role for Actions Not Submitted to Congress

Another issue concerns the treatment of rules that were never submitted to Congress. My colleague Professor Dooling has written about the role of GAO as an increasingly important actor in the CRA process—even though the CRA does not formally task GAO with producing opinions for Congress. In cases where an agency does not submit a regulatory action to Congress, members have oftentimes requested a formal opinion from GAO with regards to whether the action qualifies as a “rule” under the CRA. Whenever GAO has identified a regulatory action as a rule for purposes of the CRA, the decision is published in the Congressional Record—at which point a window opens for expedited review of the rule under the CRA. One of the more interesting examples relates to a guidance document published by the Consumer Financial Protection Bureau (CFPB) under the Obama administration in 2013. In response to a request by Senator Toomey in 2017, GAO concluded that the guidance document—which had not been submitted to Congress—qualified as a rule under the CRA. This decision initiated a review window which Congress used to nullify the CFPB guidance document. Relatedly, the current version of the draft ACUS recommendations encourage Congress to codify the process members use to seek opinions from GAO to determine what actions are “rules” under the CRA in cases where the agency did not submit the regulatory action to Congress. Interestingly, the November 4th draft ACUS recommendations suggest Congress impose a deadline for its members to request a decision from GAO to avoid instances where Congress might “subject a decades-old action to CRA review.”

Technical Reform of the CRA

Altogether, the November 4th draft ACUS recommendation is characteristic of the agency’s mission to elicit expertise in the service of improving administrative processes. The report produced by Professor Cross addresses several historical issues related to the implementation of the CRA, and it provides a thorough analysis of potential solutions available to Congress to address these issues. Each of the recommendations contained within the November 4th draft have the potential to improve the way that agencies and Congress implement the CRA.

View additional content on the Congressional Review Act.