The Brookings Institution’s Center on Regulation and Markets recently released a report examining President Trump’s Executive Order 13771, which imposed “one-in-two-out” and regulatory budget requirements. While numerous commentaries have either applauded or critiqued the Order, the Brookings report offers an objective and scholarly analysis of its possible motivations, as well as expected challenges and possible scenarios for its implementation.

Rationale for a regulatory budget

Most economists would argue that optimal policy maximizes net benefits to society, so a new regulation that offers more benefits than costs should be undertaken, whatever its contributions to the aggregate regulatory cost to society. So why is a regulatory budget needed? The Brookings report offers an explicit explanation on this:

The justification for a regulatory budget, however, is that the real-world political economy of the regulatory policymaking process deviates from the conceptual ideal of maximizing net social benefits, leading to an inefficiently high burden from regulations. The main reason why the regulatory policymaking process might fall short of the conceptual ideal is that regulators are subject to public choice incentives that can make them prone to errors or misuse of the benefit-cost approach in regulatory decision-making.

Therefore, the justification for a regulatory budget is political rather than economic. The regulatory budget, like the fiscal budget, adds a constraint that can counter those public choice incentives and, if it is implemented appropriately, could help agencies prioritize regulations, and choose those that are most effective. Indeed, the idea of regulatory budget has been discussed in academia and put into practice by other countries for some time.

Trump’s ambitious regulatory budget

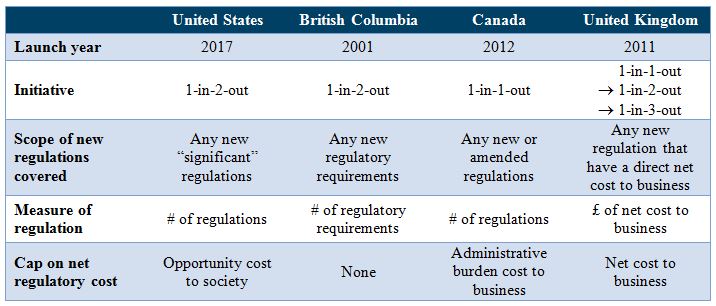

Upon reviewing the regulatory budget plans in Canada and the United Kingdom, the report calls President Trump’s plan “the most ambitious regulatory budgeting program in human history,” as it attempts to control the opportunity cost of regulation. The Canadian one-for-one rule focuses on paperwork burdens and the UK one-in-three-out policy counts business compliance costs. Opportunity cost is a much larger concept than compliance or private cost to business, since it refers to the costs to society of opportunities foregone as a result of the regulation. It is thus a more meaningful measure, but more complex and harder to estimate accurately, requiring more data, assumptions, and analysis.

Although the Trump administration narrows the scope of new regulations covered to “significant regulatory actions” as defined in Executive Order 12866, it still implies approximately 300 regulations that need to be offset every year, according to our working paper.

Challenges ahead

Among the critical legal and practical challenges discussed in the Brookings report, the most fundamental question is how to measure costs of existing regulations. The report urges the Office of Management and Budget (OMB) to develop a detailed guide to define ambiguous methodological issues such as the treatment of indirect costs, transfers, and “negative costs.” However, an OMB guide will not solve all the problems.

Evaluating costs of existing regulations is challenging primarily because the counterfactual world does not exist—we never know what would have happened if the regulation was not implemented. Fortunately, program evaluators and economists have attempted to tackle this issue for decades, and various techniques, such as randomized controlled trial and regression discontinuity design, have been developed and employed in many circumstances. But unfortunately, those techniques have not traditionally been applied to evaluate regulatory impacts.

In the program evaluation field, evaluation is mostly planed at the outset of the program, so that the theory of change that outlines the causal linkages between the intervention and the intended results as well as the measurable indicators to assess performance are predefined to enable targeted data collection and analysis during the program implementation. Some programs are even intentionally designed as experiments to understand the impact of certain types of interventions.

Such practice has not been common for regulation, and retrospective analysis has received insufficient attention and resources. Our previous review suggests that many regulations were not designed to gather the essential data to measure the intended (and unintended) outcomes for a scientific evaluation. As Susan Dudley has indicated, planning for retrospective review at the outset of the regulation is important for tackling these methodological challenges.

Facing these fundamental challenges in evaluating existing regulations, a possible pitfall in President Trump’s regulatory budget is that agencies may tend to focus on the set of regulations that is most “easy” to be repealed or revised to comply with the regulatory budget requirement, while those regulations may or may not be the most burdensome ones that should be considered for deregulation. This echoes the concern of “imprecision, inconsistency, and misuse by the agencies” raised in the report.

Net benefit principle

Since President Carter, every president in the United States has emphasized the importance of “maximizing net benefits” when developing regulations. President Trump’s regulatory reform does not necessarily alter that principle, but Executive Order 13771 puts an unprecedented emphasis on costs. As the Brookings report observes, adding a budget constraint on top of a net benefit requirement could motivate agencies to prioritize their regulatory efforts, maximizing the net benefits to society, but it could also lead to the undesirable elimination of regulations that have high costs but positive net benefits.